Understanding Cash Value in Life Insurance

Cash value life insurance is a type of permanent life insurance that provides both a death benefit and a savings component. Unlike term life insurance, which only lasts for a set period, cash value life insurance stays in effect for the policyholder’s entire life as long as the premiums are paid. Over time, the policy builds cash value, which can be used in different ways.

How Cash Value Works

Cash value is the savings portion of a life insurance policy. A portion of the premiums you pay goes toward the death benefit (the money paid to beneficiaries after your passing), while another portion is saved and grows over time. This savings can be accessed while you are still alive, making it a valuable financial tool.

The money in the cash value account grows at a set or variable interest rate, depending on the type of policy. You can use this cash for various financial needs, such as borrowing against it, withdrawing a portion, or even using it to pay future premiums. However, taking money from the cash value may reduce the death benefit your loved ones receive.

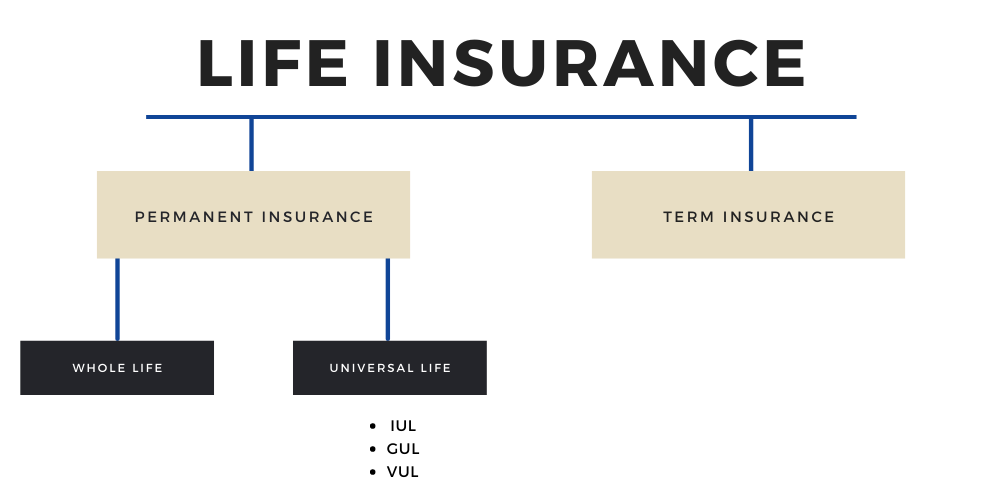

Types of Cash Value Life Insurance

There are different types of cash value life insurance, each with its own features and benefits.

1. Whole Life Insurance

Whole life insurance provides fixed premiums, a guaranteed death benefit, and a steady cash value growth. The insurance company determines the interest rate, and the policyholder does not have to manage the investments. This type of policy is ideal for those who prefer stability and predictable growth.

2. Universal Life Insurance

Universal life insurance offers more flexibility than whole life insurance. Policyholders can adjust their premium payments and death benefits within certain limits. The cash value earns interest based on current market rates, which can change over time. This option is good for those who want some control over their policy and the potential for higher returns.

3. Variable Life Insurance

Variable life insurance allows policyholders to invest their cash value in different options like stocks, bonds, or mutual funds. This means there is potential for higher growth, but also more risk. If the investments perform well, the cash value increases significantly. However, if they perform poorly, the cash value and even the death benefit may decrease.

Benefits of Cash Value Life Insurance

Having a cash value life insurance policy offers several financial benefits:

1. Builds a Financial Reserve

Over time, the policy accumulates cash value, which can be used for various financial needs. This can serve as an emergency fund, help with retirement planning, or even cover unexpected expenses.

2. Tax-Deferred Growth

The cash value grows without being taxed until it is withdrawn. This means you can accumulate savings without worrying about immediate tax payments, allowing the money to grow more efficiently over time.

3. Access to Funds

You can borrow against the cash value or withdraw money when needed. This can be useful for major life expenses such as paying for a home, education, or medical bills. However, loans and withdrawals can reduce the death benefit, so they should be used carefully.

4. Lifetime Coverage

Unlike term life insurance, which expires after a set number of years, cash value life insurance provides coverage for your entire life. As long as you continue to pay the premiums, your beneficiaries will receive a death benefit when you pass away.

Things to Consider Before Choosing a Cash Value Policy

While cash value life insurance has many advantages, it is important to consider certain factors before purchasing a policy:

- Higher Premiums – Cash value policies usually have higher premiums than term life insurance because they include a savings component.

- Slow Growth – In the early years, the cash value grows slowly because a significant portion of the premiums goes toward administrative fees and the cost of insurance.

- Fees and Charges – Some policies have fees for withdrawing or borrowing money from the cash value, and unpaid loans may reduce the death benefit.

- Not Always the Best Investment Option – While cash value life insurance offers a way to save money, other investment options like stocks or retirement accounts may provide better returns.

Is Cash Value Life Insurance Right for You?

Cash value life insurance is a good choice for people looking for lifelong coverage and a way to build savings. It works well for those who want to:

- Have permanent life insurance coverage

- Build a financial reserve for future needs

- Take advantage of tax-deferred savings

- Have flexible financial options in case of emergencies

However, if you are only looking for affordable coverage for a specific period, term life insurance may be a better option.

Conclusion:

Cash value life insurance is a long-term financial tool that provides both insurance coverage and a savings component. It offers flexibility and potential benefits, but it is essential to understand how it works before deciding if it fits your financial goals. By considering your needs, budget, and future plans, you can determine whether this type of policy is right for you.