Protection for You and Your Vehicle:

Car insurance is an essential part of vehicle ownership, offering both financial protection and peace of mind in the event of accidents, theft, or other unfortunate incidents. Whether you’re a new driver or an experienced one, understanding the different types of car insurance, how premiums are calculated, and how to choose the right coverage can save you money and ensure you are adequately protected.

What Is Car Insurance?

Car insurance is a contract between a vehicle owner and an insurance company. In exchange for regular premium payments, the insurer provides coverage for financial losses that might arise from incidents such as accidents, theft, vandalism, or natural disasters. Insurance policies vary widely in terms of coverage options, but all are designed to shield the driver and others from the financial impact of various risks.

In many regions, car insurance is a legal requirement, but even if it weren’t, having the right coverage is a smart financial decision. It not only protects you from the high costs associated with car accidents but also provides legal protection if you’re responsible for damages or injuries.

Types of Car Insurance Coverage:

Car insurance policies can be tailored to your specific needs, depending on factors such as the value of your car, where you live, and your driving habits. The main types of coverage are:

1. Liability Insurance

Liability insurance is typically mandatory and provides coverage when you’re at fault in an accident. It consists of two main components:

- Bodily Injury Liability (BIL): This covers medical expenses for injuries sustained by others in an accident you cause. It may also cover legal fees if the injured party decides to sue you.

- Property Damage Liability (PDL): This covers the repair or replacement costs for any property you damage, such as another vehicle, a fence, or a building, when you’re responsible for the accident.

Liability coverage ensures you don’t bear the financial burden of paying for others’ damages, but it does not cover your own vehicle or medical expenses.

2. Collision Insurance

Collision coverage helps pay for repairs to your car after an accident, regardless of who is at fault. Whether you collide with another vehicle, a fence, or a tree, collision coverage ensures your car is repaired or replaced. While not mandatory, collision insurance is recommended for newer or more valuable cars.

3. Comprehensive Insurance

Comprehensive coverage provides protection for non-collision-related damages. It covers events such as theft, vandalism, fire, flooding, and damage caused by animals. If you live in an area prone to natural disasters, theft, or vandalism, comprehensive insurance can be a lifesaver.

4. Personal Injury Protection (PIP)

Personal Injury Protection, also known as PIP, pays for medical expenses, lost wages, and other associated costs for you and your passengers, regardless of who caused the accident. It can be especially useful in accidents involving severe injuries or when medical bills are high.

5. Uninsured/Underinsured Motorist Coverage

Uninsured/Underinsured Motorist (UM/UIM) coverage protects you if you’re in an accident caused by a driver with insufficient or no insurance coverage. UM/UIM insurance can help cover your medical expenses and vehicle repairs, as well as any damages you may incur.

6. Medical Payments Coverage (MedPay)

MedPay is similar to PIP but usually only covers medical expenses. It can be used to pay for medical bills for you and your passengers, regardless of fault, and may also cover ambulance services and other emergency costs.

Factors That Influence Car Insurance Premiums:

Several factors affect how much you will pay for car insurance. Insurers evaluate these factors to determine the risk they are taking on by insuring you. Here are the key elements that influence your premium:

1. Driving Record

One of the most important factors in determining your premium is your driving history. A clean driving record with no accidents or traffic violations indicates that you are a lower risk to insure, and therefore, you’ll likely pay lower premiums. Conversely, if you have a history of accidents or violations, your premiums will likely be higher.

2. Age and Gender

Younger drivers, particularly those under 25, tend to pay higher premiums due to their higher risk of accidents. Statistically, male drivers are also more likely to be involved in accidents than females, which can result in higher premiums for men.

3. Vehicle Type

The make, model, and year of your vehicle play a significant role in your insurance premium. Expensive cars, sports cars, and luxury vehicles typically cost more to insure because they are more costly to repair or replace in the event of an accident. On the other hand, vehicles with good safety ratings or lower repair costs often lead to lower premiums.

4. Location

Where you live can also affect your premium. Urban areas with heavy traffic, higher crime rates, and increased risk of accidents often have higher premiums. If you live in a rural area, your rates may be lower due to less congestion and fewer accidents.

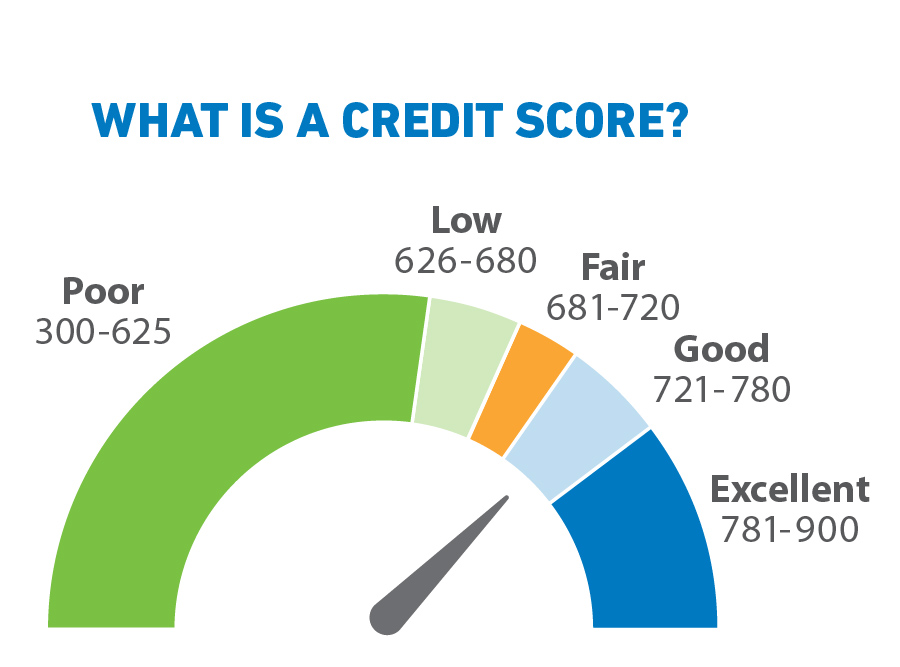

5. Credit Score

In some areas, insurers use your credit score to help determine your premium. A higher credit score suggests you’re a more responsible individual, making you less likely to file claims, which could result in lower premiums. Conversely, a low credit score can increase your premium.

6. Coverage and Deductibles

The coverage options you select and the amount of your deductible will impact your premium. Higher coverage limits typically come with higher premiums. Likewise, selecting a lower deductible may increase your premium, but it will reduce your out-of-pocket expenses in the event of a claim.

How to Choose the Right Car Insurance:

Choosing the right car insurance policy requires careful consideration. Here are some tips to help you make an informed decision:

1. Assess Your Coverage Needs

Evaluate the value of your car and your driving habits. If your car is older or has a low market value, you may not need comprehensive or collision coverage. However, if you drive frequently or your car is worth a significant amount, you may want to opt for higher coverage.

2. Compare Multiple Quotes

Don’t settle for the first quote you receive. Different insurers offer different rates and coverage options, so it’s important to shop around and compare quotes from multiple companies to find the best deal.

3. Consider Discounts

Many insurers offer discounts that can reduce your premium. These may include discounts for a clean driving record, bundling auto and home insurance, having an anti-theft device in your car, or being a member of certain organizations. Be sure to ask about all available discounts.

4. Check Insurer Reputation

When selecting an insurer, it’s important to consider their reputation for customer service, claims handling, and overall reliability. Research reviews and ratings from other customers to ensure the company is trustworthy and responsive.

5. Understand Your Policy

Before signing a contract, make sure you fully understand the terms and conditions of your policy. Review the coverage limits, deductibles, and exclusions to ensure there are no surprises later.

The Importance of Car Insurance:

Car insurance isn’t just a legal requirement in many places; it’s also a critical financial safety net for drivers. Car accidents and other unexpected incidents can result in significant financial burdens. Without adequate insurance coverage, you could be left with hefty repair bills, medical costs, or legal fees that can quickly become unmanageable.

Having car insurance also protects other people on the road. If you cause an accident, liability coverage ensures that you’re financially responsible for any damage or injuries sustained by others. Furthermore, it provides peace of mind knowing that you’re protected from potentially devastating financial losses.

Conclusion:

In conclusion, car insurance is an indispensable part of responsible vehicle ownership. By understanding the various types of coverage available, how premiums are calculated, and how to choose the right policy for your needs, you can protect yourself, your passengers, and your vehicle from unexpected risks. Carefully evaluate your options, shop around for quotes, and always opt for a policy that provides the best balance of coverage and cost for your situation.